With most of the insurance cost spikes stemming from 2020, the global pandemic is not the only thing to blame for reporting year-after-year increases in insurance costs. Rises in building materials and construction plus severe weather events resulting in property losses have also contributed. This has made it difficult for multifamily investors to see the types of passive returns they once did.

According to Forbes, the cost of living crisis is escalating the prices for everyday goods and services across the board, and insurance premiums are no exception.

The National Multifamily Housing Council’s Risk Survey for 2023 notes that insurance costs have surged 26% year over year.

And this is not just happening at home but around the globe. In Australia, even with insurer profits rising to a five-year high in 2022, KPMG predicts that premiums will rise by another 10% this year. Making it almost impossible for our friends down under to avoid being thrust into a recession.

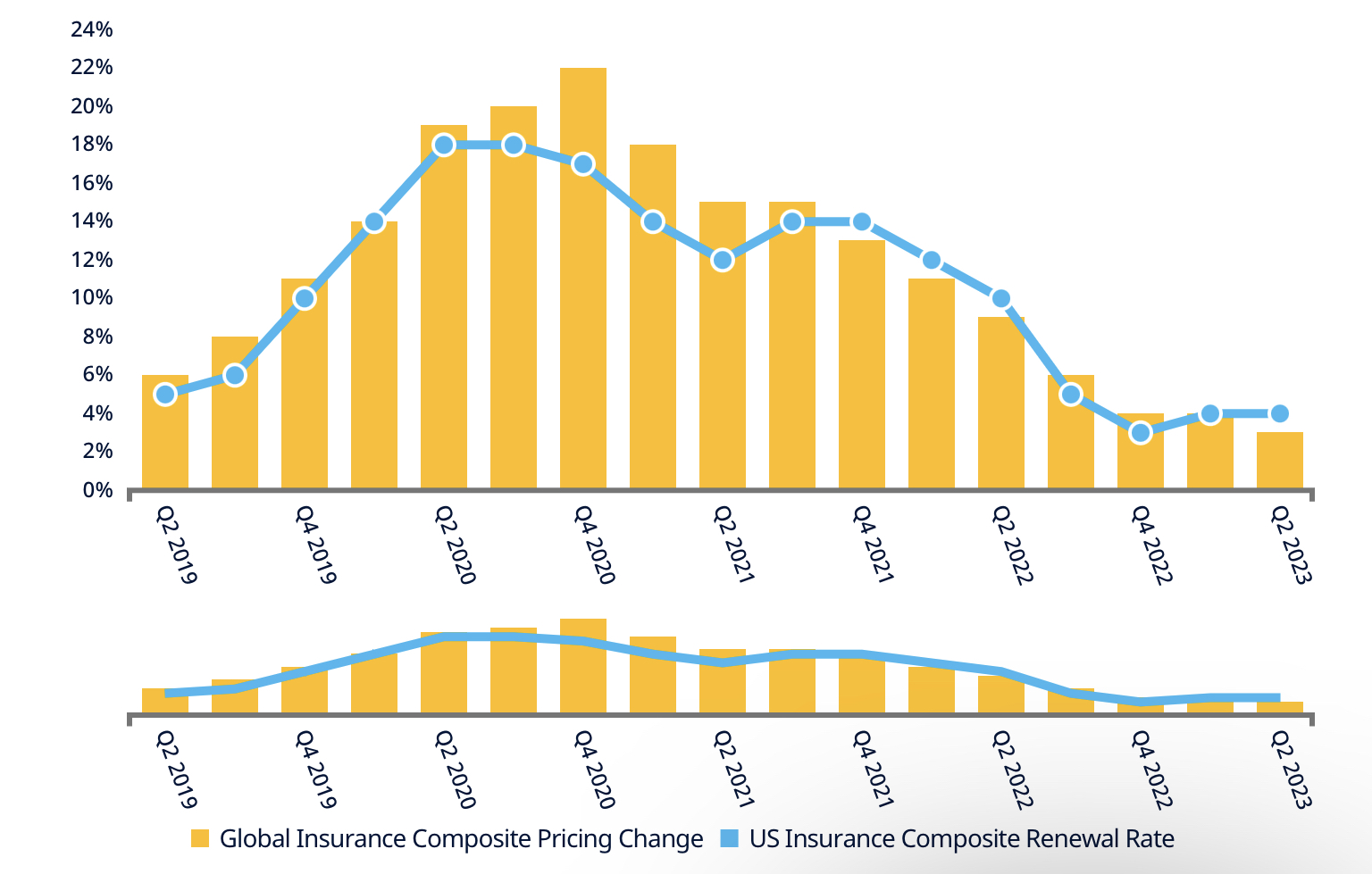

Global commercial insurance pricing rose 4% in the first quarter of 2023, the same as in the prior quarter, according to the Marsh Global Insurance Market Index.

This was the twenty-second consecutive quarter in which composite pricing rose, continuing the longest run of rate increases since the inception of the index in 2012.

From Good to Bad, Make Sure Your Seat Belt Is Securely Fastened

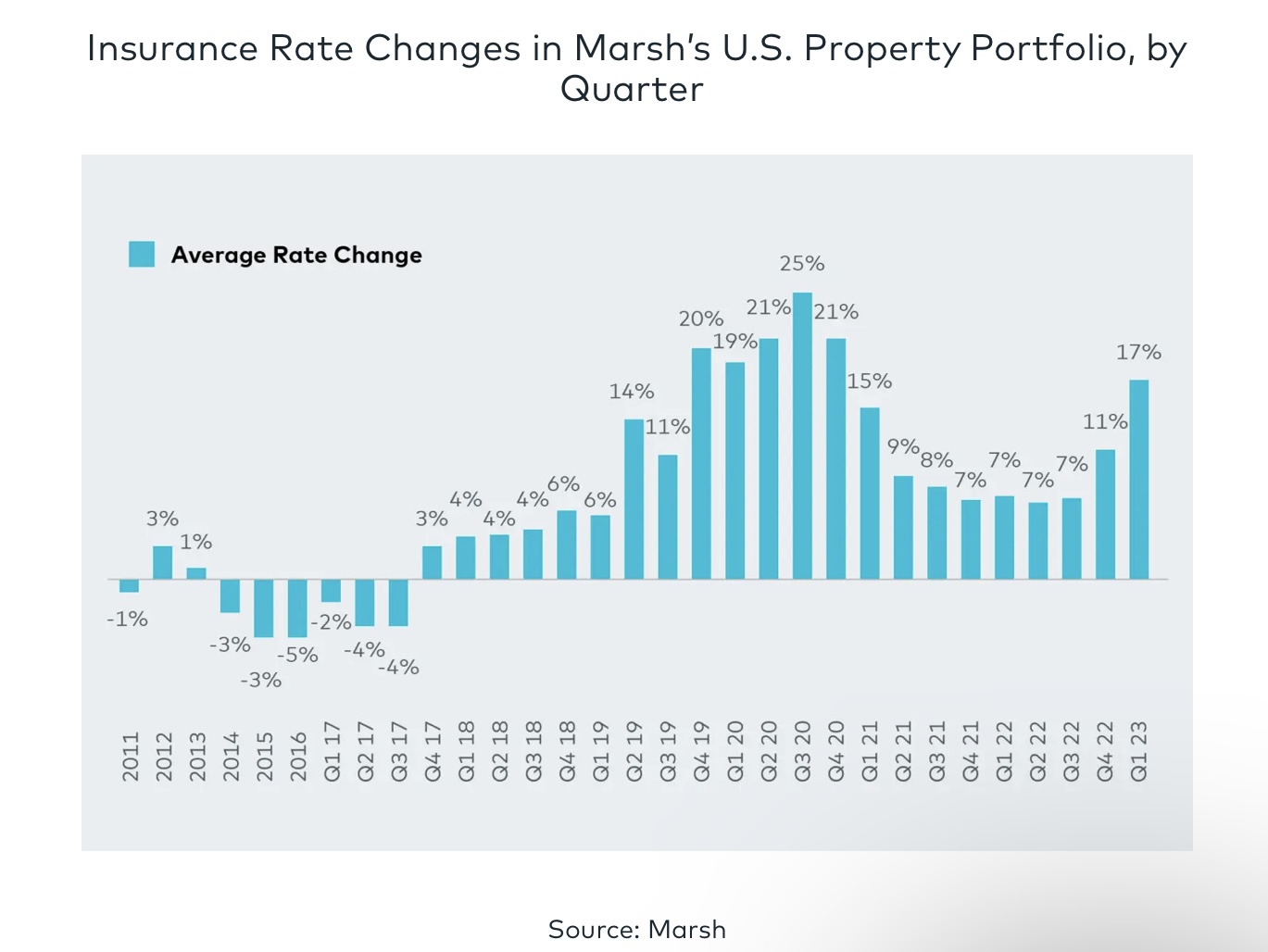

There has been a growing frequency of weather-related events causing substantial losses like Hurricane Ian which desecrated a large amount of the coastline in SW Florida in 2022. Inflation is having a major impact on commercial insurance rates by increasing claim costs, operational expenses, and reinsurance costs. We are seeing higher premiums for policyholders as insurers try to maintain profitability. Take a look at the quarter-by-quarter rate changes.

Other Factors Contributing to Inflation That May Affect the Next Decade

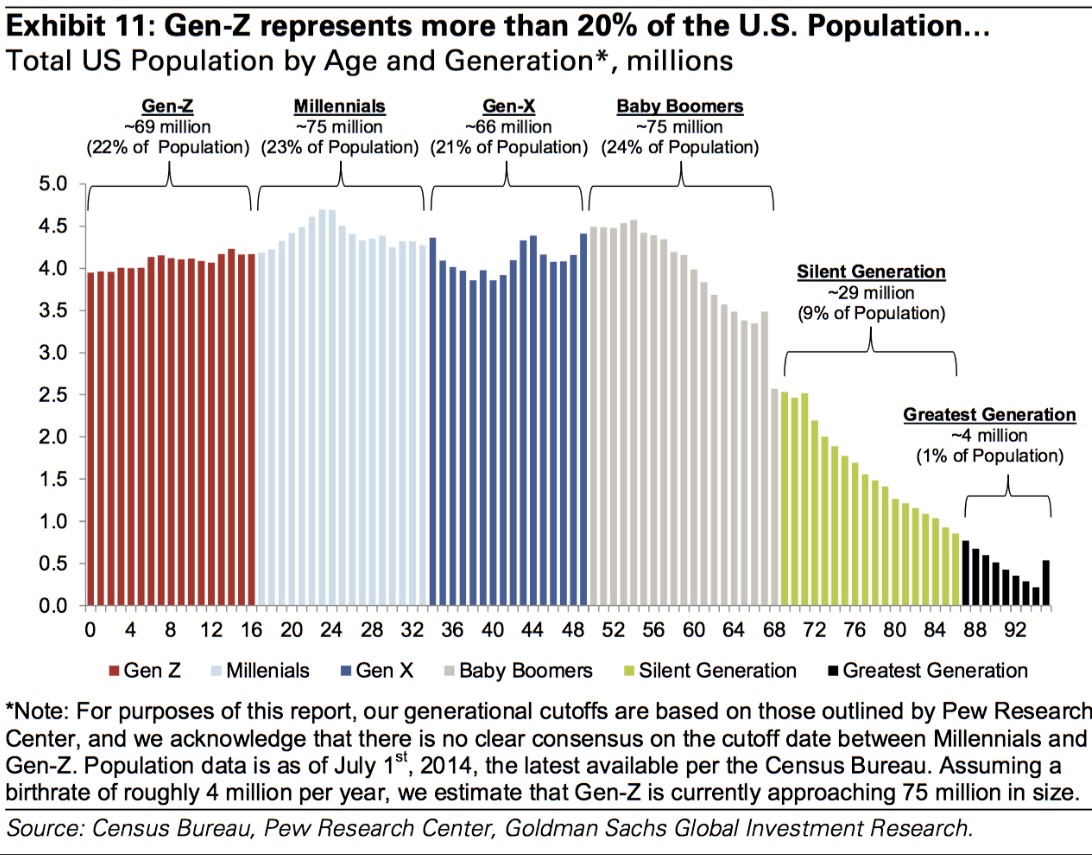

There are other factors that will continue to contribute to inflation as Baby Boomers are leaving the workforce in large numbers and jobs are not being replaced fast enough… or at all. In fact, we are seeing a deficit of approximately 400,000 jobs that have not yet been replaced.

As Boomers continue to retire this number will increase. The concern is that the generation responsible for filling these positions will fall on Generation Z. This is a slightly smaller generation but it has been said that while the most educated, Generation Z is the least likely to have work motivation compared to other generations. So, the question remains, who will fill these jobs as they continue to open?

Recession Resistant Investments

Real Estate in general and particularly multifamily real estate is still at the top of the list as a top asset class to invest in through these uncertain times. While we are not unaffected, there is proof that we are more protected by having a tangible investment that has stood the test of time.

So, it is important that we understand what types of proactive measures we can take to mitigate our risk with insurance costs on the rise and no end in the foreseeable future. With our multifamily investments, one of the things we can do to prevent being hindered by these rate increases is to be very conservative with our underwriting process so we can weather the storm and continue to see cash flow.

We Are Working to Keep Insurance at the Best Possible Rates

Here are the 7 ways Apta Properties are mitigating the higher premiums and rising costs of insurance. Taking this very proactive approach is making a difference.

- Pricing the insurance BEFORE we make an offer on a property. We want to know that the insurance rates on a property are not astronomical before we buy the asset.

- We take a deep and thorough dive into the property’s flood zones, crime, and loss runs before we purchase. All of these factors are not just clues but main points of focus that we know to look into that greatly affect insurance premiums.

- We time our renewals differently. By simply moving all of our renewals to December we are able to avoid some of the potential for rising costs due to weather. Having the renewals placed at the end of the year allows for the time to have passed from the wind season which runs through September. By moving these dates, we have moved the discussion for higher rates off the table if a storm season is bad in any particular year.

- Confirm that all valuations on the property are accurate. Since pricing for insurance is based on the Total Insurable Value (TIV) times rate, if we can keep the TIV down we create a trickle effect that keeps the overall insurance lower for the property.

- Going straight to the decision makers desk! We meet with the insurance carriers every single quarter to inform them of the preventative programs we have in place to mitigate future losses. This includes providing them with all of the items we do for risk management. We actively look for trip hazards, place stickers and send notices out if patios or balconies have grills and we make sure that residents are complying with the rules of the property with safety in mind.

- Review any open losses to confirm that we and the carrier have the correct estimated loss amounts. This helps keep the loss history as clean as possible as we go into future renewals.

- We work with known entities for Property Management companies. Because of that, they have industry best practices in place for risk management, that carriers put a premium on.

Our team has years of experience, over $1 billion in transactions and has never lost a dollar. Because of our experience we have been able to mitigate the risk of investing to ensure you see that return in your bank account. If you are interested in learning firsthand about all the positive results Apta has provided to people like you, just click the link below and learn more.